In the digital world, social proof is a powerful and effective way of boosting sales and expanding a service’s user base. People naturally look to other users for cues on how to behave—especially in uncertain or unfamiliar situations. The financial industry—particularly creators of mobile-banking apps—has embraced this strategy to drive growth. Banking is highly sensitive to trust factors, so social proof plays a critical role in customers’ decision making by providing reassurance and validation for their choices.

Popular approaches to social proof include ratings, reviews, and customer testimonials. However, online-banking services do not universally apply these common techniques, and their effectiveness varies across cultures. In this column, I’ll explore how cultural differences influence users’ behaviors relating to social proof within the context of online-banking services. Plus, I’ll provide examples from both Western and Eastern perspectives to illustrate the role that social proofs play.

Champion Advertisement

Continue Reading…

Before delving into this topic, it’s important to recognize that discussions on cultural differences are often oversimplified or generalized. To address this concern, I have compiled specific, relevant case studies that offer a thorough demonstration of the points that I’ll be discussing in this column.

The Role of Social Proof in Online Banking

To explore how cultural differences impact the application of social proof in banking, it is important to first highlight why social proof is so critical in this field. With online banking becoming ubiquitous, organizations have to nurture trust and address customer psychology, especially considering the risks and the lack of transparency in the online world. Social proof is well positioned to address their concerns. Social proof reassures customers and validates services by allowing customers to learn from others’ experience and feedback. Once customers trust a service, they are more likely to remain loyal over time. The more engaged customers are, the greater the lifetime value they provide. And the banking industry is no exception to this general rule. Statistics show that fully engaged customers contribute 37% more annual revenue to their primary bank in comparison to customers who are disengaged. Therefore, earning customers’ trust plays a significant role in a business’s long-term success.

Cultural Differences in Trust and Their Implications for Social Proof in Online Banking

Cultural factors can significantly affect how people perceive social proofs. According to Hofstadter’s framework, collective cultures such as those in Asian countries tend to tightly integrate individuals into in-groups. As a result, people often base their decisions on group thinking and community value. Let’s consider some effective social-proof techniques that online banking services in Asia employ.

MYbank, which Alibaba owns in partnership with Alipay in China, prominently features the phrase “A bank used by over 100 million people” on its hero banner, as Figure 1 shows. Their goal is to persuade people to join their service by utilizing the bandwagon effect, in which seeing many others taking the same action influences people to act. This behavior is more pronounced in collective societies. Phrases such as "trusted by millions" naturally prompt people to believe that if many others are using a service, it’s the right choice.

Figure 1—MYbank’s landing page in Alipay’s app

Referrals

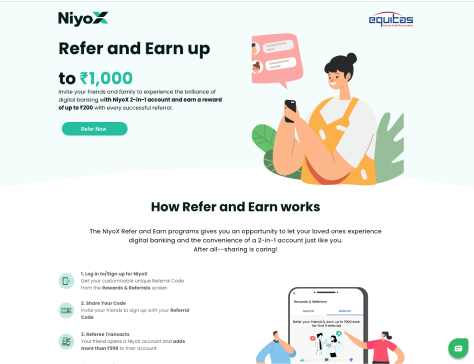

Niyo—an India-based digital banking service that is known for its travel-friendly global cards that offer no forex markup, free international ATM withdrawals, and lounge access—launched a referral program for their premium service, Niyo X. As Figure 2 shows, the program emphasizes the value it brings to customers’ loved ones and promotes the idea that sharing is caring. Niyo leverages the principle of trust in peer recommendations. People are more likely to trust suggestions from friends and family than advertisements.

Figure 2—Niyo X’s referral program

Group Accounts

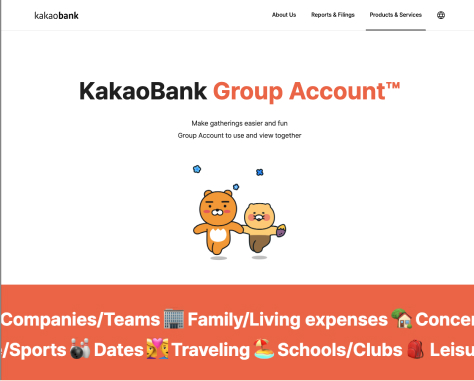

KaKao Pay, a Korean based banking service, features group-account functionality and leverages collective participation to build trust and grow its user base, as Figure 3 shows. A group account, in comparison to other forms of social proof, is slightly more indirect. However, when friends and family participate in a group account, this reinforces the perception that the service is trustworthy and reliable. A group account highlights collective activity such as shared expenses and pooling money for travel, which implies in-group validation—that is, “if others are using this service, it must be good.”

Figure 3—KaKao Pay’s group account

While Asian collectivist cultures focus on group behaviors, individualist cultures such as those in North America and Western Europe tend to prioritize personal reviews or expert endorsements, aligning with their emphasis on the I versus the We perspective. Although the nature of social proof involves group thinking, people in individualist cultures have more confidence in their personal decisions. Therefore, the types of social proof that that are prevalent among online-banking services in these regions also reflect this characteristic.

Influencer Endorsements

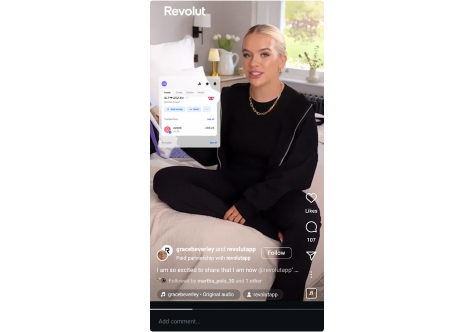

Revolut, a UK based neobank, uses endorsements from personal-finance experts and social-media influencers who discuss their experiences in using the service. These testimonials appeal to people who value personal authority and seek advice from trusted sources. One example is their partnership with Grace Beverley, a UK-based influencer and entrepreneur, who promoted their features through her Instagram account, as shown in Figure 4.

Figure 4—Revolut’s partnership with an influencer

Customer Reviews and Personal Testimonials

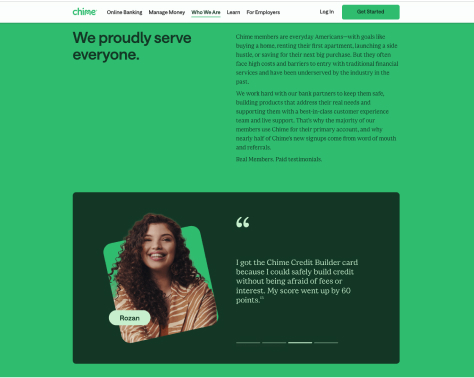

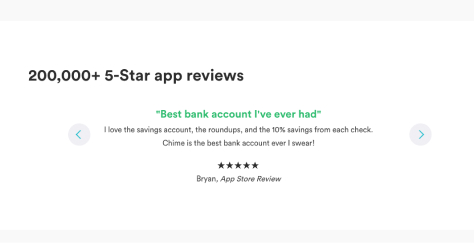

Chime, a mobile-banking service in the US, promotes customers’ individual reviews and personal testimonials on their Web site and app, as Figure 5 shows. This technique highlights how people can benefit from features such as no fees, mobile banking, and automated-savings tools. It also aligns with the individualistic value of making personal and well-informed decisions based on personal experiences.

Figure 5—Customer testimonials on Chime’s Web site

Personal Success Stories

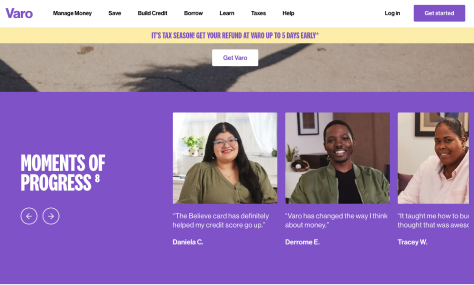

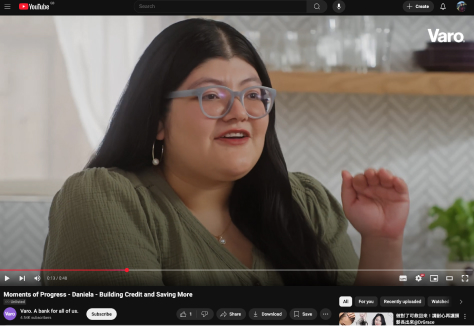

Varo, another US online-banking company, showcases the stories of individual customers who have achieved their financial goals—for example, budgeting, savings, and credit building—using their service. Figures 6 and 7 illustrate how Varo demonstrates an in-depth understanding of their customers’ stories. Telling personal success stories aligns with the individualistic values of self-achievement and financial empowerment for others who are pursuing similar goals.

Figure 6—Varo showcasing a series of success stories from customers Figure 7—An interview with one of Varo’s customers

The Evolution and Diversification of Social Proof Across Cultures: The Line Is Blurring

Although I’ve provided specific examples of social proof from both Asian and Western countries, this does not mean that these techniques cannot overlap or be used together across cultures. As Figure 8 shows, Chime’s landing page that appears when a user clicks a search ad demonstrates the effectiveness of both the wisdom-of-the-crowd approach that collectivist cultures emphasize and the personal reviews that individualist cultures prefer. Showing a significant number of 5-star reviews in combination with individual customer reviews lets visitors understand that a product provides value to others, ultimately convincing them to become users.

Figure 8—Social-proof elements on Chime’s post-click landing page

Companies can leverage social proof in a wide variety of creative ways to increase customer engagement and foster loyalty. Since banking apps typically handle sensitive financial information, understanding these cultural nuances is crucial to ensuring that the social-proof strategies that companies use in product development or global marketing are culturally appropriate and effective.

References

Jen Cardello. “Social Proof in UX.” Nielsen Norman Group, October 19, 2019. Retrieved January 20, 2025.

Susan Sorenson and Amy Adkins. “Why Customer Engagement Matters.” Gallup Business Journal, September 19, 2014. Retrieved January 20, 2025.

Jo is a product designer who has experience in various markets. She has worked in countries such as Taiwan, China, the Netherlands, and the United Kingdom. Jo has a keen interest in exploring how different cultures intersect and influence the software user interface (UI), user experience, and product strategy. Over the years, Jo has gained valuable insights from these diverse cultures and their transitions. As a result, she aims to share these insights with a broader audience that is interested in the cultural aspects of digital product design. Read More